Font size:

Print

Automotive Industry: Powering India’s Participation in Global Value Chains

India’s Automotive Drive into Global Value Chains

Context: NITI Aayog has recently launched the report “Automotive Industry: Powering India’s Participation in Global Value Chains”.

More on News:

- The report highlights India’s strategic vision to transform into a global manufacturing hub in the automotive sector, with a clear roadmap to enhance its participation in the Global Value Chains (GVCs).

- The goal is to increase India’s GVC share from 3% to 8% by 2030, supported by improved manufacturing, R&D, infrastructure, and skill development.

India’s Automotive Landscape:

- Current Position and Potential: Global Automotive Production (2023): ~94 million vehicles; global component market: USD 2 trillion; exports: USD 700 billion.

- India’s Position:

India’s Ambitions by 2030

- Automotive Component Production Target: USD 145 billion.

- Export Target: USD 60 billion, up from current USD 20 billion.

- Trade Surplus: ~USD 25 billion.

- Employment Generation: Additional 2–2.5 million jobs; total direct employment to rise to 3–4 million.

- GVC Share Increase: From 3% to 8%.

- 4th largest automobile producer globally (after China, USA, Japan).

- Production capacity: ~6 million vehicles/year.

- Strong performance in small cars and utility vehicles segments.

- Backed by policies like ‘Make in India’ and a cost-competitive workforce, India is emerging as a critical player in global automotive manufacturing and exports.

Emerging Trends Reshaping the Global Automotive Industry

- Transition to Electric Vehicles (EVs):

- Driven by sustainability concerns, emission norms, and battery tech.

- Boosts demand for lithium and cobalt—reshaping supply chains.

- Rise of Industry 4.0:

- Integration of AI, ML, IoT, Robotics.

- Leads to smart factories, improved flexibility, productivity, and cost-efficiency.

- Promotes new models like connected vehicles and digitised manufacturing.

Challenges in India’s Automotive Sector

- Low Global Component Trade Share: Just ~3% (USD 20 billion) of the global USD 700 billion export market.

- Weakness in High-Precision Segments: Only 2–4% share in engine components, transmission, and steering systems.

- Operational and Structural Constraints:

- High operational costs.

- Infrastructural bottlenecks.

- Low R&D investment (particularly in MSMEs).

- Moderate GVC integration and limited brand recognition globally.

India and the Global Automotive Value Chain (GVC)

The global automotive industry is undergoing a profound transformation driven by shifts in supply chain strategies like China+1 and Europe+1, along with the rise of electric vehicles (EVs) and increasing geopolitical uncertainties. Amidst this churn, India is emerging as a potential hub in the global automotive value chain (GVC), but significant challenges remain.

Why Global OEMs Are Looking at India

- Geopolitical Realignment: China+1 and Europe+1

- Global OEMs are increasingly diversifying production beyond China due to:

- Rising geopolitical tensions (US-China trade war, Taiwan issue).

- COVID-19 supply chain disruptions.

- Rising labour costs and regulatory scrutiny in China.

- Similarly, the Europe+1 strategy, accelerated by the Russia-Ukraine war, is driving European OEMs to seek cost-effective production bases in stable economies like India.

- Global OEMs are increasingly diversifying production beyond China due to:

- India’s Strategic Strengths

- Large Domestic Market: India is the third-largest automobile market globally by sales.

- Skilled Labor and Engineering Base: Strong talent pool in mechanical and electrical engineering.

- Growing Ecosystem: Presence of global Tier-1 suppliers, expanding R&D centers.

- Policy Push: Schemes like PLI-Auto, FAME-II, and National Electric Mobility Mission Plan (NEMMP) incentivise localisation and innovation.

- EV Potential: Start-ups and conglomerates are investing in battery tech, e-2Ws, and component manufacturing.

- Current Achievements

- Export Growth: India exported over 5 million vehicles in 2022–23, largely two-wheelers and compact cars.

- R&D and Design Centers: Global players like Hyundai, Mercedes-Benz, Bosch, and Continental have R&D operations in India.

- EV Innovations: Tata Motors, Ola Electric, and Ather Energy are spearheading the affordable EV segment.

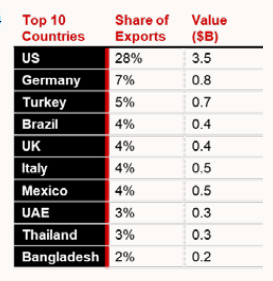

- Auto Components: India is among the top 10 suppliers of auto components globally, exporting to over 160 countries.

Proposed Interventions for GVC Integration

- Fiscal Interventions: Operational Expenditure (Opex) Support: For scaling manufacturing capabilities and Capex (e.g., tooling, dies).

- Skill Development: To create a future-ready workforce and bridge the talent gap.

- R&D and IP Transfer: Incentivising innovation and branding, Facilitating government-enabled IP transfers, especially for MSMEs.

- Cluster Development: Development of common R&D/testing facilities, Promotes collaboration, economies of scale, and supply chain resilience.

- Non-Fiscal Interventions

- Adoption of Industry 4.0:Promoting digital manufacturing and enhanced production standards.

- International Collaboration and FTAs: Encouraging joint ventures (JVs), foreign partnerships, and better market access via FTAs.

- Ease of Doing Business Reforms: Streamlining regulatory processes, Enhancing worker-hour flexibility, supplier discovery, and industrial efficiency.

Way Forward and Conclusion

- India’s automotive sector holds immense potential to become a global manufacturing leader.

- Achieving this requires:

- Center-state coordination.

- Industry participation.

- Focused investment in infrastructure, skills, and R&D.

- With the roadmap outlined in NITI Aayog’s report, India can significantly boost its exports, employment, and GVC share, leading to economic growth and global industrial leadership.